If you are looking for a credit card that rewards you every single day — not just on weekends or at specific stores — the OCBC 365 Credit Card is worth a serious look. It gives you cashback on dining, groceries, petrol, transport, bills, streaming, and even electric vehicle charging. That is a lot of ground covered by one card.

Here is everything you need to know before applying for OCBC 365 Credit Card.

OCBC 365 Credit Card: Benefits at a Glance

| Feature | Details |

|---|---|

| Highest cashback rate | 6% |

| Minimum monthly spend | S$800 / S$1,600 |

| Maximum monthly cashback | S$80 / S$160 |

| Annual income (Singaporeans/PR) | S$30,000 |

| Annual income (Foreigners) | S$45,000 |

| Annual fee | S$196.20 (first 2 years waived) |

| Annual fee waiver (subsequent years) | Min. S$10,000 spend per year |

Why the OCBC 365 Card Stands Out

More Cashback Categories Than Most Cards Will Give You

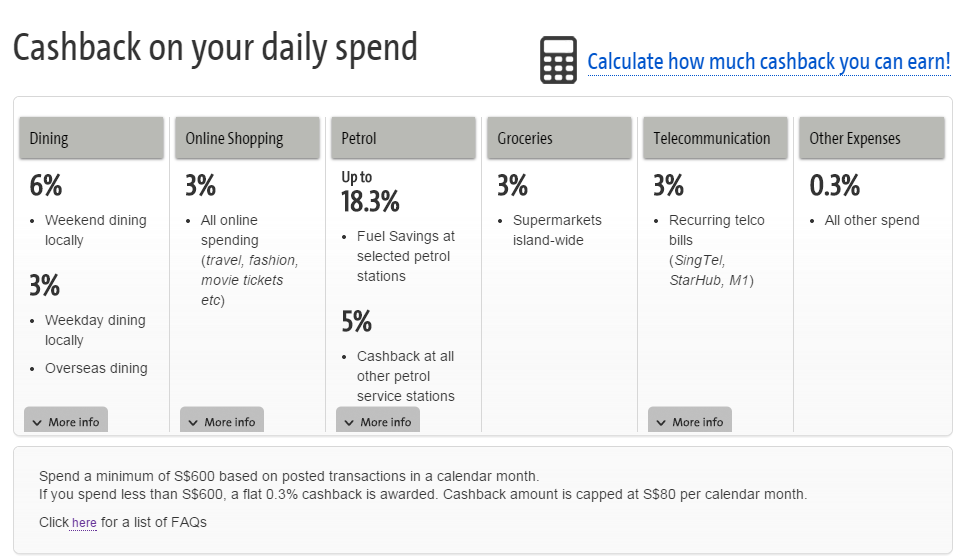

This OCBC 365 Credit Card covers more spending categories than most cashback cards in Singapore. Here is the full breakdown:

- 5% on local and overseas dining, including food delivery (GrabFood, Foodpanda, etc.)

- 6% on petrol at all service stations

- Up to 22.92% total fuel savings at Caltex (includes 18% fuel discount)

- Up to 21.04% savings at Esso

- 3% on local and overseas groceries, including Redmart and FairPrice Online

- 3% on ride-sharing — Grab, Gojek, TADA, ComfortDelGro taxis

- 3% on telco and electricity bills

- 3% on streaming subscriptions (new)

- 3% on drugstore purchases (new)

- 3% on EV charging (new)

- 0.25% on everything else

To earn these rates, you need to hit a minimum spend of S$800 in a calendar month.

Quick tip: If you want even more cashback on a wider spend range, the UOB One Card offers a base 3.33% cashback that can go as high as 15% for new UOB customers and 10% for existing ones.

The Card That Actually Works for Real Family Spending

Think about where most family money goes every month — food, groceries, Grab rides, and petrol. The OCBC 365 covers all of it without any complicated category restrictions.

Dining out as a family for S$200? That is S$10 straight back into your pocket. The 5% cashback applies every day of the week, not just weekdays or weekends. It also applies to food delivery orders, so the nights you skip cooking are covered too.

For groceries, you earn 3% back on both in-store and online orders from Redmart or FairPrice Online. Small amounts, but they add up over a year.

Earn Cashback on Bills That Most Cards Simply Ignore

Most credit cards in Singapore do not reward you for paying utility bills or telco bills. The OCBC 365 gives you 3% cashback on both.

If your monthly telco and electricity bills come to around S$200, you are looking at S$6 back each month, or S$72 a year — just from bills. That is not life-changing, but it is free money for payments you would make anyway.

No Category Restrictions on Your Cashback Cap — Spend Your Way

Many cashback cards split your cap across categories. For example, some cards let you earn a maximum of S$20 from dining, S$20 from groceries, and so on. The OCBC 365 does not work that way.

Your cashback cap is shared across all categories. So if you spend heavily on one thing — say, petrol or dining — you can still hit the full cap from just that category. This makes the card much more practical for people who do not want to micromanage their spending.

Here is how the cap works:

- Spend at least S$800 in a month → earn up to S$80 cashback

- Spend at least S$1,600 in a month → earn up to S$160 cashback

Quick tip: If most of your shopping is online or contactless, check out the UOB EVOL Card too. It gives 8% cashback on online and mobile contactless spend — no expense tracking needed.

OCBC 365 Credit Card Fees and Charges

| Fee Type | Amount |

|---|---|

| Annual fee | S$196.20 (first 2 years waived) |

| Annual fee waiver (subsequent years) | Spend S$10,000 per year from the month after card issuance |

| Late payment charge | S$100 |

| Minimum monthly payment | 3% of total balance or S$50, whichever is higher, plus overdue amounts |

| Interest on purchases | 27.78% p.a. (min. S$2.50/month) |

| Interest on cash advance | 28.92% p.a. compounding (min. S$2.50) |

| Cash advance fee | S$15 or 6% of amount, whichever is greater |

| Foreign currency transaction fee | 3.25% |

Who Can Apply for the OCBC 365 Credit Card?

- At least 21 years old

- Singaporeans and PRs: Minimum annual income of S$30,000

- Foreigners: Minimum annual income of S$45,000

Documents You Need to Apply for OCBC 365 Credit Card?

Prepare these documents beforehand:

For Singaporeans and PRs:

- Front and back of NRIC

- Salaried employees: Last 6 months’ CPF contribution history

- Self-employed or commission earners: Latest Income Tax Notice of Assessment or latest 12 months’ CPF statement

For Foreigners:

- Passport and Employment Pass

- Latest computerised payslip and Income Tax Notice of Assessment, or a company letter confirming employment and salary

So, Should You Get the OCBC 365 Credit Card?

For most people in Singapore, yes. The OCBC 365 is not flashy — it does not come with airport lounge access or miles — but it does something more useful for day-to-day life: it gives you real money back on the things you actually buy every week.

The 6% petrol cashback is one of the strongest fuel rewards available right now. The 5% dining cashback applies any day of the week, not just on specific days. And the new additions — streaming, drugstore, EV charging — make the card feel current rather than dated.

The deal-breaker to watch out for is the S$800 minimum monthly spend. Fall below that in any given month and you get 0.25% on everything. For a single person with low fixed expenses, that can be a problem. For a household managing groceries, bills, transport, and dining — S$800 disappears fast.

The cap doubling from S$80 to S$160 is a real improvement. If you spend S$1,600 or more a month, this card rewards you more than it used to.

OCBC 365 Credit Card: Pros & Cons

Pros

- 6% cashback on petrol at all service stations

- 5% cashback on dining and food delivery, every day of the week

- 3% cashback on groceries, transport, telco, electricity, streaming, drugstore, and EV charging

- Cashback cap is not locked to specific categories — spend how you want

- Monthly cashback cap raised to S$160

Cons

- Minimum S$800 monthly spend required to unlock higher cashback rates

- Only 0.25% cashback if you spend below S$800 in a month

- 0.25% cashback on all other categories not listed above

Final Take: Expert Review

If your monthly card spend clears S$800 and most of it goes toward food, fuel, transport, or bills — this card puts more cash back in your pocket than most others on the market.

From my personal take the OCBC 365 Credit Card is worth it for the Singapore’s user and this card make a sence for the user who spend there money on movie, shopping, and more.