I still remember when credit cards felt risky in small Indian towns. Nobody trusted them. People thought you’d end up in debt before the month was over. But after using cards for a few years now, I’ve figured out one thing — the best card isn’t always the fanciest one. Sometimes it’s just the one that quietly saves you money every single month. That’s the Axis Bank Ace Credit Card for me.

No five-star lounge promises. No confusing reward point math. Just straightforward cashback on the stuff you already buy — groceries, food delivery, electricity bills, cab rides. If that sounds boring, it also sounds like money back in your pocket.

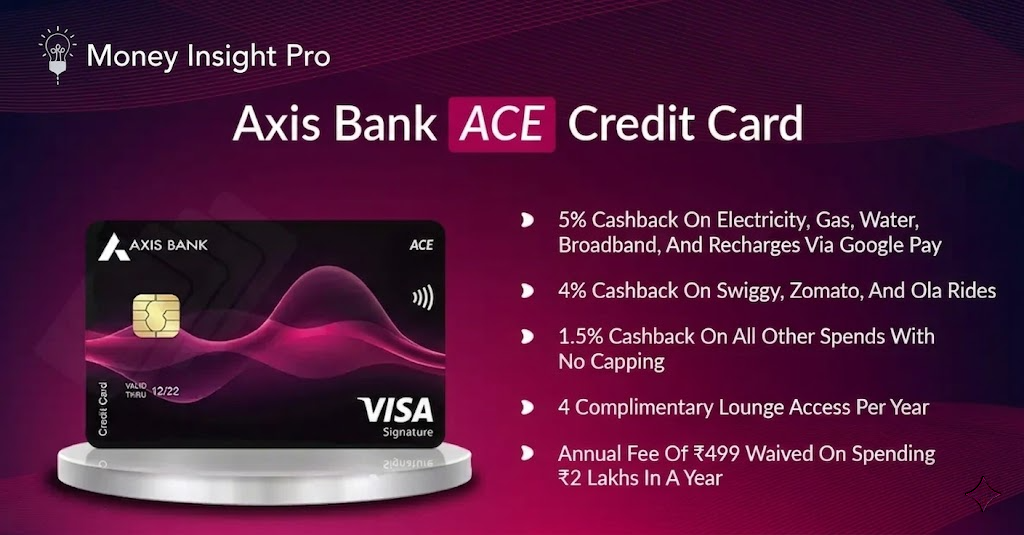

Axis Bank Ace Credit Card: Full Details at a Glance

Before we get into the good stuff, here’s a quick look at what the card actually offers:

- Card Network: Visa.

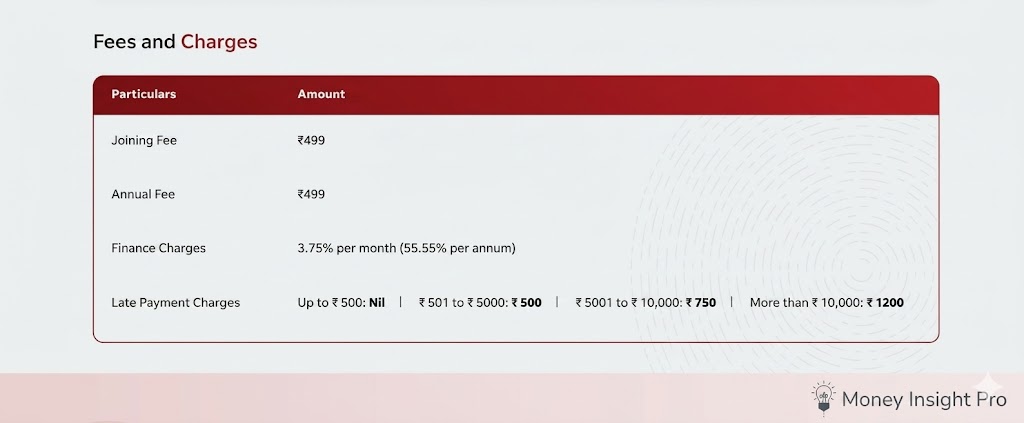

- Joining Fee: ₹499.

- Best Cashback Rate: 5% on utility bills and mobile recharges paid via Google Pay.

- Monthly Cashback Cap: ₹500 per billing cycle on Google Pay and Swiggy.

- Food and Rides: 4% cashback on Swiggy and Ola.

- Everything Else: 1.5% cashback on all other spends.

- Lounge Access: 4 free domestic visits per year (you need to spend ₹50,000 in the last 3 months to unlock this).

- Annual Fee: ₹499 — can be waived if you spend ₹10,000 in the first 45 days (check the offer at the time you apply).

- Fuel Benefit: 1% surcharge waiver on fuel spends between ₹400 and ₹4,000 — capped at ₹500 a month.

Axis Ace Credit Card Cashback Rates Explained Simply

Here’s the cashback breakdown in plain language:

| What You Spend On | Cashback You Get | One Thing to Keep in Mind |

|---|---|---|

| Utility bills and recharges via Google Pay | 5% | Must be paid directly in the GPay app — not through another wallet |

| Food delivery and rides (Swiggy, Zomato, Ola) | 4% | Only for online orders — offline restaurant bills don’t count |

| All other purchases | 1.5%–2% | No minimum spend, cashback added directly to your statement |

The 5% Google Pay cashback is the biggest reason people pick this card. But there’s one thing I always tell people: make sure the payment is going directly through GPay. If it gets routed through PhonePe or another wallet, the cashback won’t apply. It’s a small thing but worth knowing upfront.

Dining, Airport Lounge, and Fuel Benefits — Are They Worth It?

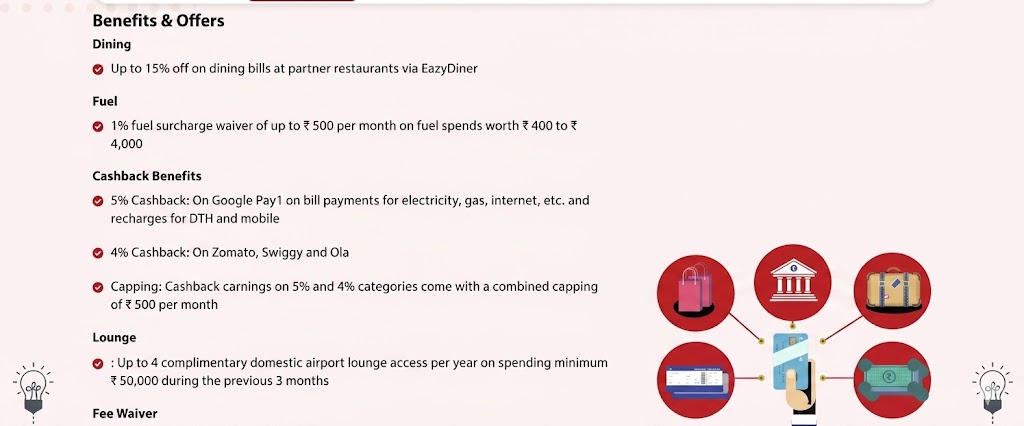

Dining Discounts at Popular Restaurants with Axis Ace Card

You get up to 20% off at partner restaurants — KFC, TGI Fridays, Tossin Pizza, Chicago Pizza are some names on the list. This works twice a month and saves you up to ₹1,000 per visit. If you eat out even once a month at these places, that’s a nice bonus on top of the cashback.

Free Airport Lounge Access for Domestic Travelers

Four free domestic lounge visits per year. To unlock this, you need to spend ₹50,000 in the three months before your trip. If you travel every quarter for work or holidays, hitting ₹50,000 is very doable. And getting even two or three lounge visits free from a ₹499-a-year card? That’s a solid deal.

Fuel Surcharge Waiver for Daily Commuters

Fill up between ₹400 and ₹4,000 and you skip the 1% fuel surcharge. Maximum saving is ₹500 a month. It’s not a big number, but it’s free money for something you were already paying for.

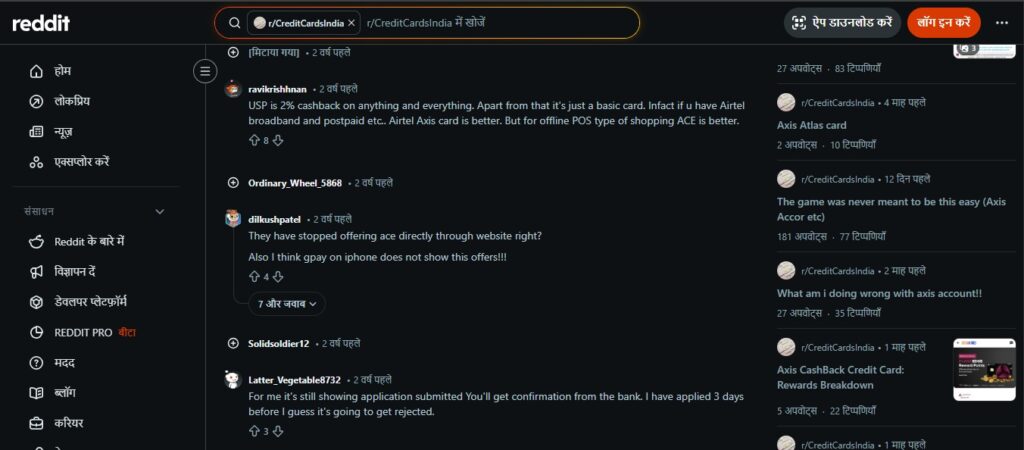

What People on Reddit Are Actually Saying About This Card

I spent some time going through r/CreditCardsIndia to see what real users think — not the polished stuff on brand websites.

Here’s what I found:

- Getting approved is relatively easy. A lot of first-time credit card users said they got approved smoothly through the digital application. That’s a big plus if you’re just starting your credit journey.

- The cashback is easy to understand. Most users said they appreciate that they can actually see the cashback in rupees on their statement. No point conversion. No wondering what 500 reward points are worth.

- The main complaints? Some users mentioned delays in credit bureau updates after getting the card. A few said approval decisions felt random — approved one time, rejected another, with no clear reason.

One comment summed up the general feeling nicely: “5% on GPay, 4% on food and rides, 1.5–2% on everything else. No mental gymnastics.”…..That’s about right.

Who Is the Axis Bank Ace Credit Card Really For?

Honestly? This Axis Bank Ace Credit Card is made for the average Indian household.

If your month looks like this — pay electricity bill, order dinner on Swiggy, book an Ola, pay the mobile recharge — you’ll get value from this card without doing anything extra. It just runs in the background and gives you money back.

I’d especially recommend it for people spending somewhere between ₹15,000 and ₹30,000 a month. That’s the sweet spot where the cashback really adds up but you’re not overspending just to hit some milestone.

This is also a great first credit card. The benefits are simple enough that you won’t get confused, and the cashback is real — it shows up as rupees on your statement, not points that expire in six months.

Axis Bank Ace Credit Card Pros and Cons: Honest Take

The good stuff:

- Cashback on the categories most people actually use every day

- 4% on food delivery and cab rides is higher than most cards in this price range

- Cashback hits your statement as real rupees — you don’t need to do anything to use it

The not-so-good stuff:

- ₹499 annual fee isn’t automatically waived for everyone

- Approvals can feel a bit inconsistent — some people get approved easily, others don’t, and Axis doesn’t always explain why

- There’s no cashback for grocery shopping or big retail purchases, which is a gap for many families

Does the ₹499 Annual Fee Actually Pay for Itself?

Short answer: yes, in the first month.

If you pay ₹10,000 in utility bills through Google Pay every month, that’s ₹500 cashback right there — which already covers the yearly fee. Over 12 months, that’s ₹6,000 in cashback from just one spend category.

And the rest of your spending? That’s extra on top.

Even if most of your spending is in the 1.5% general category, you’ll still recover the fee without breaking a sweat.

Real Monthly Cashback Calculation for Axis Ace Card

Let’s say you spend ₹15,000 a month, spread across three categories:

| Spend Category | Monthly Amount | Cashback Rate | Cashback Earned |

|---|---|---|---|

| Google Pay bills and recharges | ₹5,000 | 5% | ₹250 |

| Food delivery and cab rides | ₹5,000 | 4% | ₹200 |

| Other purchases | ₹5,000 | 1.5% | ₹75 |

| Total | ₹15,000 | — | ₹525/month |

That’s ₹6,300 back every year on completely normal spending. The ₹499 annual fee pays for itself in the first month and then some.

Axis Ace vs Amazon Pay ICICI vs HDFC Millennia: Which One Wins?

Axis Ace Credit Card vs Amazon Pay ICICI Card

Amazon Pay ICICI is excellent — but mainly if you shop on Amazon a lot. Step outside Amazon and the benefits shrink fast. Axis Ace covers a wider spread of everyday spending, so it works better for people who don’t live on Amazon.

Axis Ace Credit Card vs HDFC Millennia Card

HDFC Millennia runs on a reward points system. Points sound exciting until you realize they expire quickly and the redemption process takes effort. Axis Ace skips all that. The cashback is direct and immediate.

If simplicity matters to you, Axis Ace is the easier choice here.

My Personal Rating for Axis Bank Ace Credit Card

| What I Checked | My Score (Out of 20) | My Reasoning |

|---|---|---|

| Daily Spend Coverage | 18/20 | Hits most categories well — grocery is the only real miss |

| Value for Monthly Spend | 16/20 | Works best between ₹15,000–₹25,000 per month |

| Good as a First Card | 19/20 | Simple, honest benefits — perfect for beginners |

| Does It Deliver What It Promises | 20/20 | Promises cashback. Gives cashback. That’s it. |

| Fee vs What You Get Back | 17/20 | Fee recovers fast, though easier waiver conditions would be nicer |

| Overall | 90/100 | A solid everyday card that does what it says |

Common Axis Ace Card Problems — and Easy Fixes

Cashback Not Showing Up Correctly?

Open Google Pay and check which payment method is selected. It should show “Axis Bank Ace Credit Card” directly — not another wallet with your Axis card behind it. That’s the most common reason cashback gets missed.

Credit Score Not Updated After Getting the Card?

Give it two full billing cycles. Then check your score on both CIBIL and Experian. If it’s still not showing, reach out to Axis Bank customer care with your statement.

Not Sure If Your Annual Fee Was Waived?

Axis sometimes auto-waives the fee after your first qualifying spend, but this is linked to specific offers at the time of application. Don’t assume it applies — track your first-year offer carefully.

Should You Get the Axis Bank Ace Credit Card? My Final Answer

Look, if you’re searching for premium travel cards or fancy lifestyle perks, this isn’t your card. There are better options for that.

But if you just want a card that saves you money every month without making you think too hard — this one does the job really well. Pay your bills, order food, book a cab. The cashback just happens. You don’t manage it.

It works great as your main card and also as a backup card if you already have something else. The key question is: how much of your spending happens online? If 30–50% or more is digital — especially through Google Pay — you’ll see real savings from month one.

For most people living in Indian cities today, that’s exactly how things already work.

Frequently Asked Questions About Axis Bank Ace Credit Card

No, it has a ₹499 annual fee. But it may be reversed through promotional offers — check at the time you apply.

You don’t need to redeem or convert anything. The cashback just shows up on your statement as a rupee credit.

No. Rent payments and wallet top-ups don’t earn cashback and may come with extra charges.

Not directly as a UPI card. But you can link it inside Google Pay for bill payments and mobile recharges — that’s where the 5% cashback kicks in.

Usually by your next billing cycle, after the transaction is settled.