Let’s be honest — most Singaporeans want a card that actually helps them fly somewhere nice without draining their bank account first. And if you’ve been hunting for an air miles card that punches above its weight class, the UOB PRVI Miles Credit Card deserves a serious look.

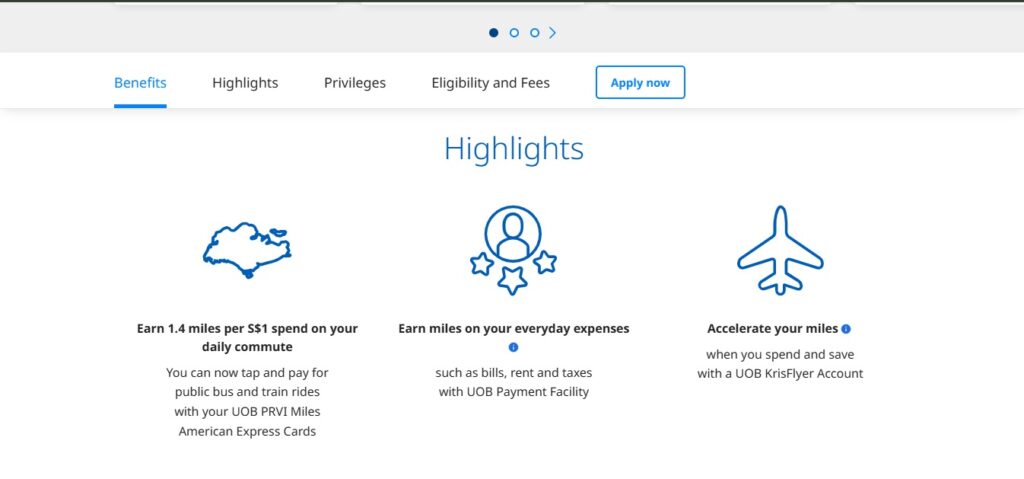

This card has been quietly earning fans — not because of flashy marketing, but because its numbers are genuinely hard to argue with. While most entry-level miles cards offer the standard S$1 = 1.2 miles on local spending, the UOB PRVI Miles Card hands you S$1 = 1.4 miles locally and a very generous S$1 = 2.4 miles overseas. Add in a low-income requirement of just S$30,000 per year, and you’ve got one of the more accessible yet rewarding miles cards in Singapore’s market right now.

Whether you’re a frequent business traveller, a family that racks up everyday local spend, or someone who simply wants more from every dollar — this card is worth your attention. Let’s dig into the details.

UOB PRVI Miles Credit Card — Fees & Charges (Full Transparency)

Before you fall in love with any card, always check the fees. Here’s exactly what the UOB PRVI Miles Card will cost you:

| Fee Type | Amount |

|---|---|

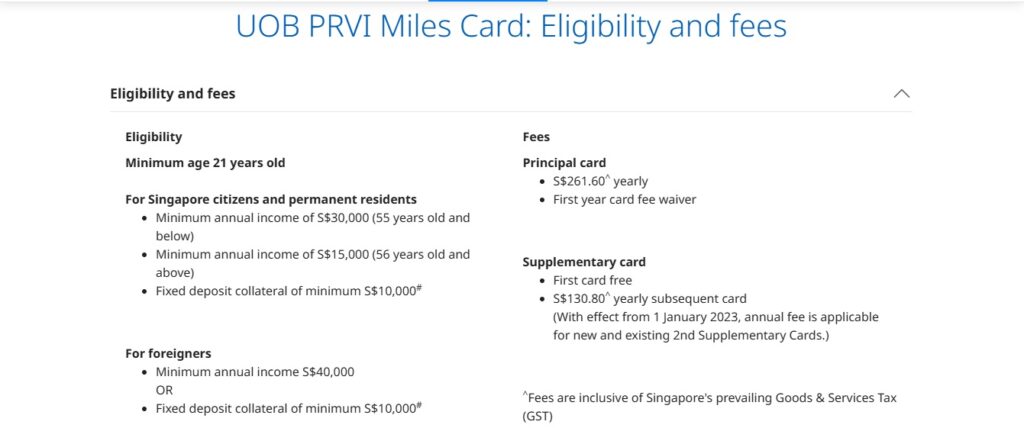

| Annual Fee (Principal Card) | S$256.80 (Waived for the first year) |

| Supplementary Cards (First 2) | Free |

| Supplementary Cards (Subsequent) | S$128.40 each |

| Annual Interest Rate | 26.90% |

| Interest-Free Period | 21 days |

| Late Payment Penalty | S$100 |

| Minimum Monthly Repayment | 3% of outstanding balance or S$50 — whichever is higher |

Important: The annual fee of S$256.80 is waived for the first year — but from Year 2 onwards, it kicks in. There is no spend-based fee waiver mentioned in the current terms. So if you’re not a big spender, factor this cost into your decision.

That said, S$256.80 is roughly the cost of two decent hotel meals. If your miles usage is consistent, you’ll likely recover this fee through the value of miles earned within the first few months.

Welcome Benefits

The UOB PRVI Miles Credit Card doesn’t splash a huge welcome bonus in your face (unlike some competitors). However, if you go for the American Express version of the card, new UOB customers are rewarded with S$100 in Grab ride credits — a nice little gift to start your relationship with the card.

This isn’t the most aggressive welcome offer in Singapore’s miles card market, but the real long-term value here lies in the earn rates — which we’re about to get into.

- Pro Tip: Never apply directly through the bank without checking these aggregator sites first. It’s free money (or stuff) for a few minutes of clicking.

Reward Structure — Where This Card Truly Shines

This is where the UOB PRVI Miles Card stops playing games and starts dominating. The earn rates are uncapped, meaning the big spenders can really clean up.

The Value of 1 Mile: First, the currency. You earn UNI$ , where 1 UNI$ = 2 miles. Generally, 10,000 miles can get you a one-way economy ticket to somewhere like Bangkok or Phuket.

How You Earn:

- Local Spend (SGD): 1.4 miles per dollar. This beats the usual “entry-level” market rate of 1.2 mpd offered by cards like the Citi PremierMiles .

- International Spend (Overseas): 2.4 miles per dollar. Again, it’s higher than the standard 2 mpd you see elsewhere .

- Online Travel (Expedia, Agoda, UOB Travel): Up to 6 miles per dollar. This is the accelerator. Booking a hotel for the weekend? Those miles add up fast. (Just note it excludes budget airlines).

- Regional Spend (AMEX Version): If you have the American Express variant, spending in Indonesia, Malaysia, Thailand, and Vietnam can earn you even more, plus you get those sweet limo transfers we’ll mention later.

The Fine Print (Human Logic):

Miles expire after two years. The bank is basically saying, “We trust you’ll travel within two years, but if you’re a slow saver, this isn’t the card for you.” Also, transactions are rounded down to the nearest S$5. A S$4.90 coffee? Zero miles. It’s annoying, but it means this card works best for consolidated spending, not micropayments.

UOB PRVI Miles Credit Card — Key Benefits & Features

Free Travel Insurance

Like most air miles cards in Singapore, the UOB PRVI Miles Card provides complimentary travel insurance — but only when you charge your entire travel fare to the card. This is a standard condition across the industry, so not unique to UOB, but still a meaningful add-on that saves you a separate insurance purchase.

The American Express Version — Extra Perks Worth Considering

If you’re open to carrying the Amex variant, there are some notable extras:

- 20,000 bonus loyalty miles every year — when you spend S$50,000 or more in a calendar year

- Up to 8 complimentary airport transfers to Changi Airport per year

- S$100 in Grab ride credits for new UOB customers

The S$50,000 annual spend milestone for the 20,000 bonus miles is a high bar — that’s a dedicated big spender’s territory. But if you’re a business owner or a high-income professional who naturally puts most expenses on a card, those 20,000 extra miles are a very generous annual loyalty reward.

8 free airport transfers per year on the Amex version is a standout feature. At typical private transfer rates in Singapore, that’s potentially S$400–S$600 in saved costs annually — almost enough to offset the annual fee on its own.

Honest Review — Pros & Cons

What We Like

- Above-market earn rates at both local and overseas tiers

- Accessible S$30,000 income requirement

- 6 miles per S$1 on travel portals is exceptional

- First 2 supplementary cards are free

- Available in Visa, Mastercard & Amex variants

- Amex version adds airport transfers & annual bonus miles

Watch Out For

- No spend-based annual fee waiver

- Miles expire after just 2 years

- 6x travel bonus excludes low-cost carriers

- High 26.90% interest rate if you carry a balance

- S$50,000 spend required for Amex loyalty miles

- Travel insurance only covers full fare charged to card

Expert Opinion — Should You Get This Card?

Here’s the honest truth: the UOB PRVI Miles Credit Card is not for everyone — but for the right person, it’s one of the best deals in Singapore’s crowded miles card space.

The S$256.80 annual fee (from Year 2) sounds like a lot until you do the math. At S$1 = 1.4 miles locally, you’d need to spend roughly S$1,820 per month just on local transactions to earn miles worth around S$257 at a conservative redemption value of 1 cent per mile. That’s achievable for most working adults who put their regular household expenses on a card.

The card really earns its keep for frequent travellers and families with high regular spending. Think of a family of four booking international flights a few times a year — between the 2.4x overseas earn rate and the 6x rate on Agoda or Expedia, miles accumulate at a pace that most cards simply can’t match at this income tier.

Also Read :- Scapia Federal Credit Card Review 2026: Zero Forex, Zero Annual Fee, Maximum Travel Value

Who Is the Ideal UOB PRVI Miles Cardholder?

- Business travellers who regularly spend overseas

- Families with large monthly local spend (groceries, dining, kids’ activities)

- People who book hotels and flights through Expedia, Agoda, or UOB Travel

- High earners (especially on the Amex variant) who can hit the S$50,000 spend milestone

- Anyone who wants a true miles card without a premium S$80,000+ income requirement

Who should skip this card?

If you rarely travel internationally, carry a monthly balance, or prefer cashback over miles — this isn’t your card. The 26.90% interest rate will quickly devour any miles value if you don’t pay in full each month. This card rewards disciplined spenders, not revolving credit users.

Conclusion & Final Verdict

The UOB PRVI Miles Credit Card remains one of the strongest air miles credit cards in Singapore, especially for travellers who want consistent mileage rewards without extremely high income requirements.

Its main strengths include:

- High miles earning rates

- Strong overseas spending rewards

- Travel booking bonus of up to 6 miles per $1

- Reasonable S$30,000 income requirement

While the annual fee and two-year miles expiry are small drawbacks, the card still delivers excellent value for people who travel frequently or spend significantly on their credit card.

If your goal is to earn airline miles faster and convert everyday spending into travel rewards, the UOB PRVI Miles Card is definitely worth considering.

FAQs About UOB PRVI Miles Credit Card

Applicants typically need a minimum annual income of S$30,000 to qualify for this credit card in Singapore.

A short-haul flight (like Singapore to Bangkok) usually costs around 10,000 miles.

1. If you spend locally (1.4 mpd), you need to spend about S$7,150.

2. If you spend overseas (2.4 mpd), you need to spend about S$4,200.

The annual fee of S$256.80 is waived for the first year. From Year 2 onwards, the fee applies. As per current terms, there is no spend-based waiver condition, so the fee is charged regardless of how much you spend.

Yes. UOB miles expire after 2 years. This is a key difference from competitors like DBS or Citi, which offer non-expiring miles.

The earn rates are similar, but the AMEX version offers exclusive perks: up to 8 complimentary airport limo transfers per year and a 20,000 miles loyalty bonus if you spend S$50,000+ in a year. The downside? Not every merchant accepts AMEX.

If you don’t have the 6,500 UNI$ (13,000 miles) to cover the fee, UOB will deduct half from your miles and bill you the remaining half in cash.