The Scapia Credit Card is a Lifetime Free (LTF) travel card with zero forex markup, unlimited domestic lounge access, and 10–20% Scapia coins on all spends. Backed by Federal Bank and Bank of Baroda. New applicants must apply through the BOB Scapia variant (Federal Bank cards are currently paused by RBI).

Why Is Everyone Talking About the Scapia Credit Card?

But the thing is with 2026. More and more people are traveling than ever before. Flights are getting cheaper and cheaper. Even young professionals are taking international flights as part of their vacations. But still, one thing bothers us. The additional charges that are levied on the credit card when used outside the country.

Usually, every credit card charges us 3.5% on every international transaction done using the credit card. So, if you are using your credit card on your international vacation and have spent ₹1 lakh, then you are paying ₹3,500 for no reason.

But with the Scapia credit card, this is not the case. It charges zero percent on all international transactions. Plus, there are rewards that can be redeemed to get free flights.

This is the best time to apply for this credit card as every rupee saved can be used on the vacation. Plus, the Federal Bank version is on hold, and this is the only way to get this benefit from the BOB Scapia credit card.

What Makes the Scapia Credit Card Special?

Most travel credit cards have a catch — they’re either expensive (high annual fees), restrictive (rewards only on specific categories), or both. Scapia flips that model on its head.

The Scapia Credit Card is a Lifetime Free (LTF) card, which means you pay ₹0 in annual fees, ever. There’s no spend-based waiver to chase, no renewal fee looming at the end of the year. And unlike many “travel” cards that reward you only when you book through their portal, Scapia gives you coins on every online and offline spend.

What really sets it apart is the combination: zero forex markup + unlimited domestic lounge access + LTF status. Getting even two of these three features on a free card is rare. Getting all three? That’s genuinely unusual in the Indian credit card market.

Key Features at a Glance

- Zero forex markup on all international transactions

- Unlimited domestic lounge access across India

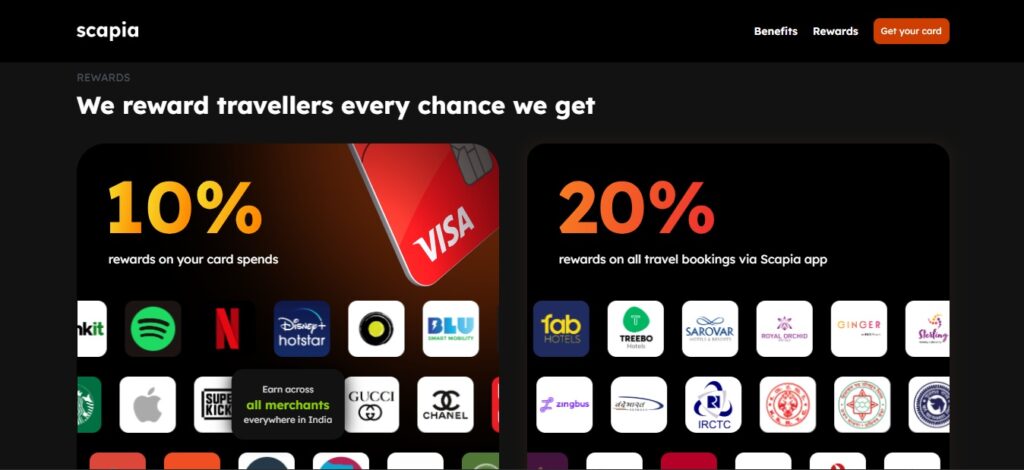

- 10% Scapia coins on all online and offline spends

- 20% Scapia coins when booking flights and hotels through the Scapia app

- No-cost EMI options available

- Lifetime Free — ₹0 annual fee, no conditions

Fees & Charges — The Transparency Section

One of the biggest trust signals for any financial product is how clearly it communicates its costs. Here’s the full picture for the Scapia Credit Card:

| Charge Type | Amount |

|---|---|

| Joining Fee | ₹0 |

| Annual Fee | ₹0 (Lifetime Free) |

| Forex Markup Fee | 0% on international transactions |

| Interest Rate (Finance Charge) | 45% p.a. (3.75% per month) |

| Cash Advance Fee | 2.5% of amount or ₹500 — whichever is higher |

| Grace Period | Up to 48 days (interest-free) |

A few things worth noting here:

On the interest rate: 45% per annum sounds alarming — and it should. This rate applies only if you carry an outstanding balance (i.e., you don’t pay your full bill by the due date). You get a generous 48-day grace period; pay in full within that window and you pay zero interest. The golden rule of credit cards applies here: never revolve a balance.

No fee waiver conditions to worry about here — it’s simply free. That’s refreshing.

Welcome Benefits — What Do You Get When You Join?

The Scapia Credit Card keeps its welcome structure simple and honest: there are no flashy sign-up vouchers or bonus points to lure you in. Instead, the value proposition is baked into the ongoing rewards system — every rupee you spend starts earning Scapia coins from day one.

Once approved, you’ll receive a virtual card within 2–5 days, which you can use immediately for online transactions and contactless payments. The physical card follows shortly after.

For a lifetime-free card, this is fair — the real “welcome benefit” is that you’re never charged to own it in the first place.

READ MORE: Scapia Federal Credit Card Review 2026: Zero Forex, Zero Annual Fee, Maximum Travel Value

Reward Structure — How Scapia Coins Actually Work

This is the heart of the Scapia Credit Card, and it’s genuinely well-designed for a travel-focused card. Every rupee you spend converts into Scapia coins, and these coins have a fixed value of ₹0.20 per coin. Here’s the full breakdown:

| Spend Type | Scapia Coins Earned | Effective Value (₹0.20/coin) |

|---|---|---|

| All online & offline spends | 10% coins | 2% return |

| Flights & hotels via Scapia App | 20% coins | 4% return |

| International spends | 10% coins + 0% forex | 2% return + saves ~3.5% |

Breaking It Down in Plain Numbers

Say you spend ₹50,000 in a month on regular purchases (groceries, online shopping, dining out). You earn 5,000 Scapia coins, worth ₹1,000 in travel redemptions. That’s a flat 2% return with no category restrictions — no “only on dining” or “only on fuel” conditions.

Now say you book flights worth ₹30,000 through the Scapia app. You earn 6,000 coins — worth ₹1,200 back in your pocket. The 4% return on travel bookings is genuinely competitive, especially for a zero-fee card.

And if you’re spending abroad — let’s say you swipe $500 at an international hotel — you’re not just earning coins on that. You’re also saving the 3.5% forex markup that most other cards would charge. On $500, that’s roughly ₹1,450 saved on forex alone, plus another ~₹690 in coin value. Total benefit? Over ₹2,100 on a single transaction.

Important: Scapia coins are redeemable only through the Scapia app for flights and hotels. They cannot be transferred to airline miles, redeemed for cashback, or used at partner brands outside the app. Keep this in mind if you prefer flexible redemptions.

Key Benefits & Features — What Else Does Scapia Credit Card Offer?

Unlimited Domestic Lounge Access

This one is genuinely impressive for a lifetime-free card. Most entry-level LTF cards either offer no lounge access or cap it at 2–4 visits per quarter. Scapia gives you unlimited domestic lounge access — which alone could justify owning this card if you travel frequently.

For context: a typical airport lounge visit costs ₹500–₹800 if you pay out of pocket. If you travel even once a month and use a lounge, you’re saving ₹6,000–₹10,000 annually — more than enough to offset any theoretical annual fee (if the card had one, which it doesn’t).

Zero Forex Markup on International Transactions

Standard credit cards in India charge a 3.5% forex markup on every international transaction. That’s basically a 3.5% surcharge on everything you buy abroad — at restaurants, hotels, online shopping from international sites, or even Netflix if your account is billed in dollars.

Scapia eliminates this completely. For a frequent international traveller or someone who shops globally online, this is a substantial saving.

No-Cost EMI

For larger purchases, Scapia credit cards offers no-cost EMI options — a feature that’s helpful if you’re making a big ticket purchase and want to split payments without paying interest. Terms and eligible merchants may vary, so always check within the app before assuming eligibility.

What This Card Doesn’t Cover

Honesty matters here. The BOB Scapia Credit Card does not offer fuel surcharge waivers, insurance covers, or milestone benefits like some premium cards do. There are also no rewards on fuel spend or rent payments. If these features are important to your lifestyle, you may want to pair Scapia with another card in your wallet.

Federal Bank Scapia Card vs BOB Scapia Card — What’s the Difference?

Both versions of the Scapia Credit Card offer identical rewards and core benefits. The differences are entirely around issuance and a couple of practical features:

| Feature | Federal Bank Scapia Card | BOB Scapia Card |

|---|---|---|

| Current Status | RBI has paused new issuances (2025) | Active — new applicants can apply |

| Add-on Cards | Yes (can add family members) | Not available |

| Best For | Existing cardholders; UPI via RuPay | All new applicants |

| Rewards & Lounge | Same as BOB variant | Same as Federal variant |

The bottom line: if you’re a new applicant, apply for the BOB Scapia Card. The RBI has paused Federal Bank’s new card issuances in 2025, so that route isn’t available for now. Existing Federal Bank Scapia cardholders will continue to be served without any disruption.

Federal Bank’s card has a slight edge if you already hold it (add-on cards for family, and UPI via RuPay), but for someone starting fresh, the BOB variant gives you everything you need.

Who Should Apply for the Scapia Credit Card?

Not every card is for everyone — and the Scapia Credit Card is refreshingly honest about its target audience.

This card is ideal for you if:

- You travel frequently — domestically or internationally

- You regularly book flights and hotels (the 4% return via the app is excellent)

- You shop on international websites or travel abroad (zero forex = real savings)

- You want lounge access without paying a ₹3,000–₹5,000 annual fee

- You’re a GenZ or millennial who prefers an app-first experience

- You want your first credit card to be low-risk (₹0 annual fee, easy approval)

This card is probably not for you if:

- You rarely travel and spend mostly on fuel, rent, or utilities

- You want rewards redeemable as cashback or Amazon/Flipkart vouchers

- You need a credit card with insurance covers or milestone benefits

- You want add-on cards for your family (BOB variant doesn’t support this)

How to Apply for the Scapia Credit Card

The application process is fully digital and takes under 10 minutes. Here’s how it works:

- Download the Scapia app from the Play Store or App Store and enter your mobile number for OTP verification.

- Fill in your personal details — PAN card, Aadhaar, and basic income information.

- Complete the Video KYC — a quick video call that usually wraps up in a few minutes.

- Wait for approval — if approved, your virtual card arrives within 2–5 days and is ready for immediate use. The physical card follows.

There’s no branch visit required, no physical paperwork, and no need to courier documents. For a generation that grew up doing everything on their phones, this process feels exactly right.

Scapia Customer Care — Getting Help When You Need It

Scapia offers 24/7 support through the app’s “Help” section with an instant chat option. For urgent issues, you can also call:

- Federal Bank Helpline: 1800-425-16666

- Bank of Baroda Helpline: 1800-5700

- Email: support@scapia.cards (replies within 24 hours)

There’s also an in-app chatbot for quick queries. Pro tip: upload a screenshot of the issue you’re facing — it speeds up resolution significantly. Always note your query/ticket number so you can track the status.

Expert Opinion: Is the Scapia Credit Card Worth It?

Let’s apply some straightforward financial logic here.

The annual fee is ₹0. So the bar for “worth it” is practically on the floor — you just need to use it at least once and it’s already cost you nothing. But beyond that baseline, the Scapia card delivers real, measurable value for the right kind of user.

Take a typical scenario: someone who travels domestically 6–8 times a year, uses airport lounges, spends about ₹30,000/month on the card, and occasionally shops on international websites. Let’s run the rough math:

- Lounge access savings: 8 visits × ₹600 average = ₹4,800/year

- Scapia coin value on ₹3,60,000 annual spend at 2%: ₹7,200

- Forex savings on international spends (estimated ₹50,000/year at 3.5%): ₹1,750

- Total estimated annual value: ₹13,750+

All of this from a card that costs you absolutely nothing. That’s not just “worth it” — that’s a genuinely strong value proposition.

The only real limitation is the travel-only redemption model. If you earn coins but don’t use the Scapia app to book travel, those coins are essentially stranded. So this card works best when your spending and your redemptions are both in the travel space. If you’re a pure cashback person, look elsewhere.

Final Verdict

Scapia Credit Card Rating: 4.3 / 5

For frequent travellers, especially those who do international transactions, this is one of the best lifetime-free cards available in India right now. The zero forex markup alone pays for itself, and unlimited lounge access on a ₹0-fee card is genuinely rare. The travel-only redemption is the one trade-off — go in knowing that, and this card will serve you very well.

Conclusion — Should You Get the Scapia Credit Card?

Here’s the short answer: if you travel even a few times a year and occasionally transact in foreign currencies, adding the Scapia Credit Card to your wallet is a no-brainer. It costs you nothing, saves you real money on forex and lounges, and rewards every rupee you spend.

For new applicants in 2025, the BOB Scapia Credit Card is your only option — and that’s perfectly fine. The rewards, lounge benefits, and zero forex features are identical to the Federal Bank version. The only thing you miss out on is add-on cards for family, which matters only if that was a priority for you.

Download the Scapia app, apply for the BOB variant, and start turning your everyday spending into free flights. In a market full of travel cards that charge ₹3,000–₹10,000 a year for similar benefits, a lifetime-free card that delivers this much value is genuinely worth your attention.

Frequently Asked Questions (FAQs)

Yes, completely. The Scapia Credit Card has a ₹0 joining fee and ₹0 annual fee, with no spend-based waiver condition. You don’t need to spend a minimum amount each year to keep the card free — it’s free regardless of your usage.

Each Scapia coin is worth ₹0.20. So if you earn 1,000 coins in a month, that equals ₹200 in travel credit, redeemable on flights or hotels booked through the Scapia app.

No — the RBI has paused new card issuances from Federal Bank’s Scapia programme as of 2025. New applicants should apply for the BOB (Bank of Baroda) Scapia Credit Card, which offers identical rewards and benefits and is currently active for new applicants.

No. Scapia coins are exclusively redeemable for flights and hotel bookings through the Scapia app. They cannot be converted to cashback, transferred to airline loyalty programmes, or used at any partner outside the Scapia platform. This is the card’s biggest trade-off — it’s purely a travel rewards card.

No — Scapia offers unlimited domestic lounge access. Whether you’re traveling once a month or every week, you can use eligible airport lounges across India without worrying about a quarterly cap.

The interest rate is 45% per annum (3.75% per month) on the outstanding balance. You get a grace period of up to 48 days — pay your full bill within this window and you pay zero interest. Always pay in full to avoid this charge.

I hope this review helps you decide if the Scapia credit card is right for you. If you already use this card, tell me about your experience in the comments. Your story might help someone else make a better choice.