If you use Paytm regularly for recharges, bill payments, or shopping, this credit card is probably worth a look. The Paytm HDFC Credit Card gives you cashback on Paytm spends, a free Paytm First membership, and a few other perks that can actually make a difference day-to-day.

Here’s a clear breakdown of what you get, what it costs, and how to apply for Paytm HDFC Credit Card.

What Do You Get with Paytm HDFC Credit Card?

The biggest draw is the cashback on Paytm. You get 3% cashback on Paytm utility payments, recharges, movie tickets, and Mini App spends — up to ₹500 per month. On other Paytm spends (like shopping), the cashback drops to 2%, also capped at ₹500 per month.

If you spend outside Paytm — at regular stores or online — you get 1% cashback, but only when your monthly spending crosses ₹10,000, and that’s capped at ₹100 per month.

Other benefits include:

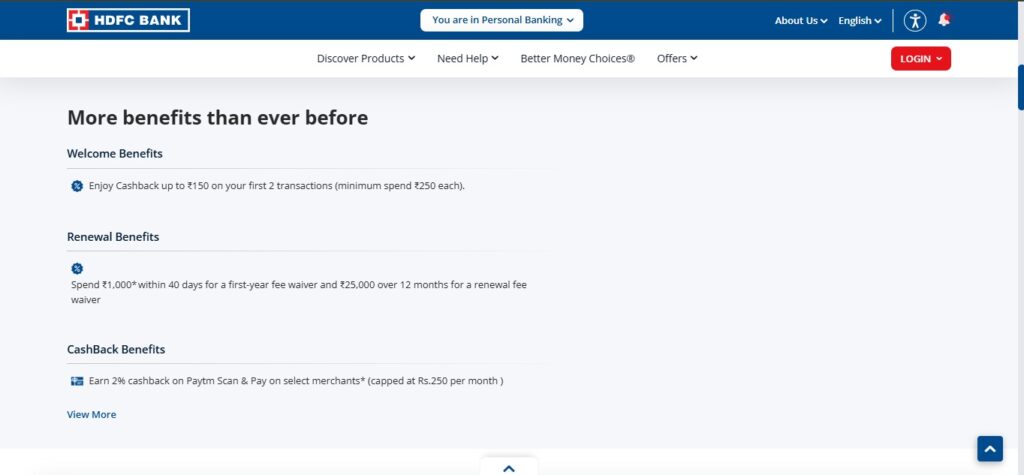

- Free Paytm First Membership after your first ₹100 transaction

- 1% fuel surcharge waiver up to ₹250 per statement cycle

- Up to 4 free add-on cards

- Automatic utility bill payments through HDFC SmartPay

- Monthly fee waiver if you spend ₹5,000 or more in a month

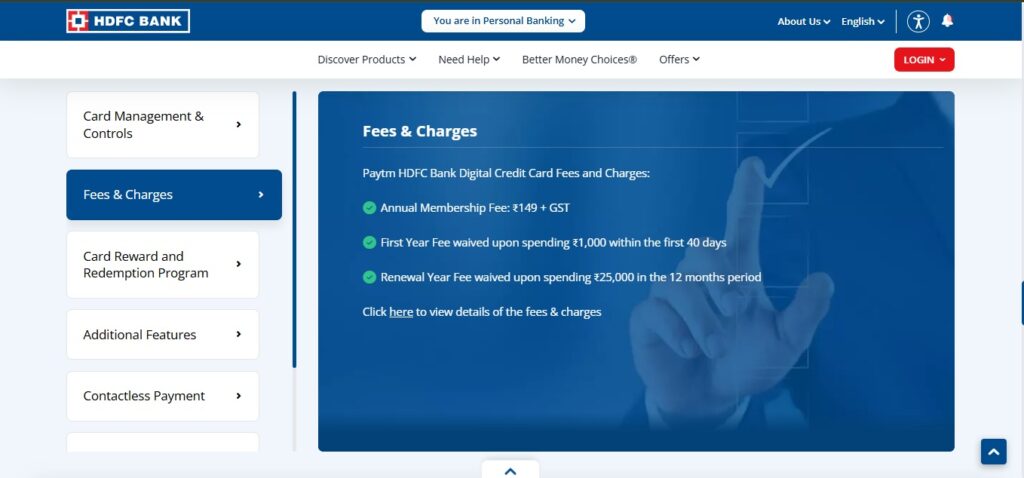

Paytm HDFC Credit Card: Charges & Fees

| Fee Type | Amount |

|---|---|

| Monthly Membership Fee | ₹49 + GST (waived on ₹5,000/month spend) |

| Annual Membership Fee | ₹500 + GST |

| First-Year Fee Waiver | Spend ₹30,000 within first 3 months |

| Renewal Fee Waiver | Spend ₹50,000 in a year |

| International Transactions | 1% markup |

| Rental Transactions | 1% (from 2nd rental transaction/month) |

| Cash Advance | 2.5% or ₹500, whichever is higher |

| Add-on Card Fee | Free (up to 4) |

| Rewards Redemption Fee | Free |

| Interest on Cash Advances | 1.99% – 3.49% per month |

One thing worth noting: the fee waivers are easy to hit if you’re already using Paytm regularly. Spending ₹5,000 in a month is not a stretch for most people.

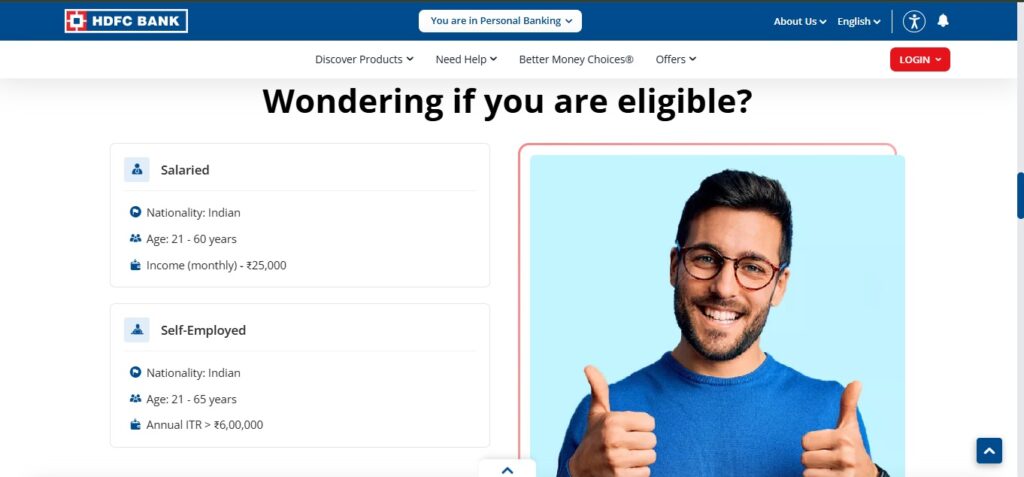

Who Can Apply for Paytm HDFC Credit Card?

This card is not open to everyone — HDFC offers it only to selected Paytm customers. The basic eligibility requirements are:

- Age: 18 to 60 years

- Regular income (salaried or self-employed)

- CIBIL score: 750 to 900

If your credit score is below 750, it’s worth working on that first before applying.

How to Apply for Paytm HDFC Credit Card?

You cannot apply directly from the HDFC website’s main credit card page. Here’s how it works:

- Go to the HDFC Bank credit card application page

- Enter your mobile number and PAN card number (or date of birth)

- Click “Get OTP” and verify

- Fill in your details and select Paytm HDFC Bank Credit Card

- Submit your application

That’s it. The process is straightforward.

What’s the Paytm HDFC Credit Card limit?

HDFC does not publish a fixed credit limit for this card. Your limit is set based on your income, occupation, and CIBIL score. If you want a higher limit, a better credit score and consistent income documentation will help.

How to Track Your Application Status

Online: Visit the HDFC Bank credit card status page and enter your mobile number, Application Reference Number (or Form Number), date of birth, and CAPTCHA. Click Submit to see your status.

By phone: Call HDFC Bank’s 24/7 customer care at 1800 202 6161 or 1860 267 6161.

Paytm HDFC Credit Card Customer Care No

| Contact | Number |

|---|---|

| Within India | 1800 202 6161 or 1860 267 6161 |

| Outside India | +91 22 6160 6161 |

How to Track Card Delivery

Once your application is approved, HDFC sends a dispatch email or letter with an Air Way Bill (AWB) number. Use this number on the HDFC tracking page to check your card’s delivery status.

How to Log In Paytm HDFC Credit Card?

The Paytm HDFC Credit Card is managed through the HDFC MyCards app, accessible only from a mobile browser (not desktop or laptop).

- Open the HDFC MyCards app on your mobile browser

- Enter your registered mobile number

- Verify with OTP

- View dues, track reward points, and redeem cashback from there

Paytm HDFC Credit Card Reward Points Value

The cashback you earn is called CashPoints. Here’s how redemption works:

- Minimum redemption: 500 CashPoints

- Against statement balance: 1 CashPoint = ₹1

- For travel (flights/hotels) or SmartBuy portal: 1 CashPoint = ₹0.30

Redeeming against your statement balance is clearly the better deal. For travel redemptions, the value drops significantly, so keep that in mind.

Is This Card Worth It?

Honestly, it depends on how much you use Paytm.

If Paytm is your go-to app for recharges, bills, and everyday payments, this card can save you a fair amount each month. The 3% cashback on Paytm spends is solid, and the free Paytm First membership adds extra offers on top of that.

If you rarely use Paytm, the benefits thin out quickly. The 1% cashback on regular retail spends is nothing special, and you’d probably get more value from a general cashback card.

The monthly fee of ₹49 is low enough that most regular Paytm users will easily offset it with cashback. Just make sure you’re spending ₹5,000 a month to keep the fee waived.

Quick Summary

| Feature | Detail |

|---|---|

| Best For | Frequent Paytm users |

| Top Cashback | 3% on Paytm utility/recharge/movies |

| Monthly Fee | ₹49 + GST (waived on ₹5,000 spend) |

| Welcome Gift | Free Paytm First Membership |

| Fuel Waiver | 1% up to ₹250/cycle |

| Add-on Cards | Up to 4, free |

| Credit Score Needed | 750–900 |

The Paytm HDFC Credit Card works best when you’re already spending on Paytm. If that’s you, the cashback and fee waivers are easy to take advantage of. If not, you might want to look at other options before applying.