Honestly, whenever I think about any credit cards, one question always comes up — am I actually getting something back from this card, or is it just another piece of plastic sitting in my wallet?

That question matters even more with the HDFC MoneyBack Credit Card. Because when a card puts the word “MoneyBack” right in its name, you expect it to deliver.

So I took a close look at how this MoneyBack Credit Card actually works. Here’s everything that matters — no fluff, no filler.

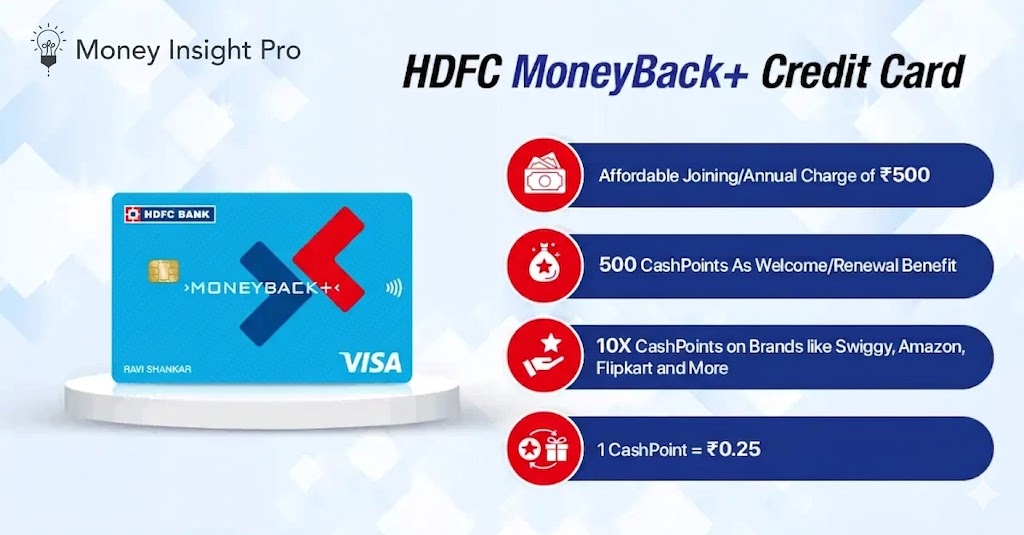

What Is the HDFC MoneyBack Credit Card?

The idea is simple. You spend, the card gives you reward points. Those points can later be turned into cashback or gift vouchers.

This card is built for people who don’t want to deal with complicated reward systems — no confusing tiers, no high annual fees, no fine print that makes your head spin. You spend on things you already buy, you earn points, you get money back.

Is it as simple as it sounds? Mostly yes — but a few things are worth understanding before you apply.

What Does the MoneyBack Credit Card Offer?

Reward Points on Every Purchase

Groceries, online shopping, utility bills — you earn points on all of it. The rate can vary depending on the category, and HDFC sometimes runs bonus point campaigns during festive seasons.

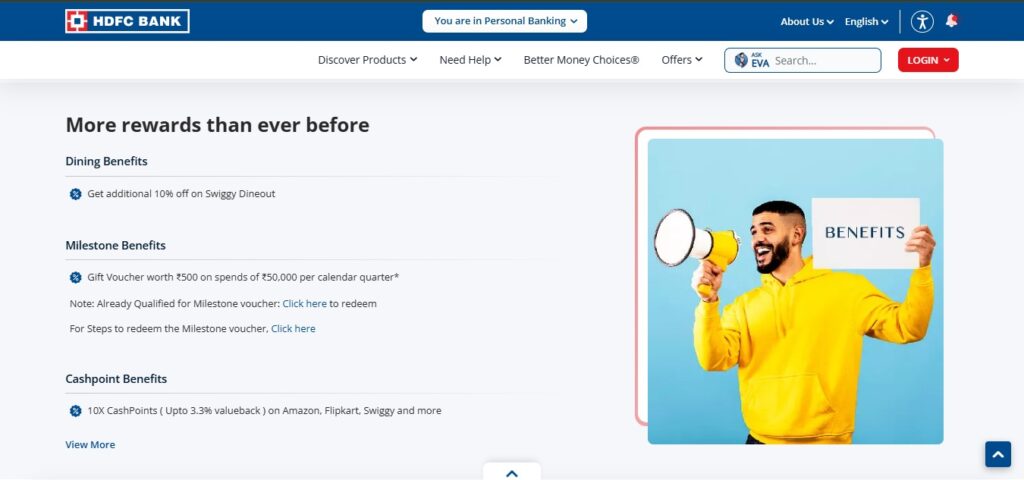

Cashback on Everyday Spending

Fuel, groceries, dining out — cashback from these categories goes directly to your account or reduces your credit card bill. If you already spend regularly in these areas, this is a genuinely useful feature.

Partner Merchant Discounts

HDFC has tie-ups with several merchants across dining, travel, and lifestyle. If you already spend at some of these places, getting a little extra discount on top is a nice bonus.

- HDFC MoneyBack Credit Card — The Cashback Secret 90% of Indians Don’t Know

- OneCard Metal Credit Card Review 2026: India’s Most Powerful Free Metal Credit Card Revealed!

- DBS Vantage Credit Card Review 2026 – Benefits, Fees & Should You Get It?

How the HDFC MoneyBack Card Rewards System Works?

Earning rewards is pretty simple:

- Every transaction gives you baseline points

- Certain categories — usually online purchases — give you more points

- Festive season promotions sometimes offer bonus points on top

When it comes to redeeming, you have a few options:

- Cashback — The most straightforward option. Convert your points to cashback and reduce your credit card bill. If you don’t want to overthink rewards, this is the way to go.

- Gift Vouchers — Useful if you prefer to redeem points for shopping or dining.

- Travel Benefits — Some points can go toward travel discounts, though this isn’t the card’s main selling point.

The flexibility is good. You can pick whatever works best for your situation.

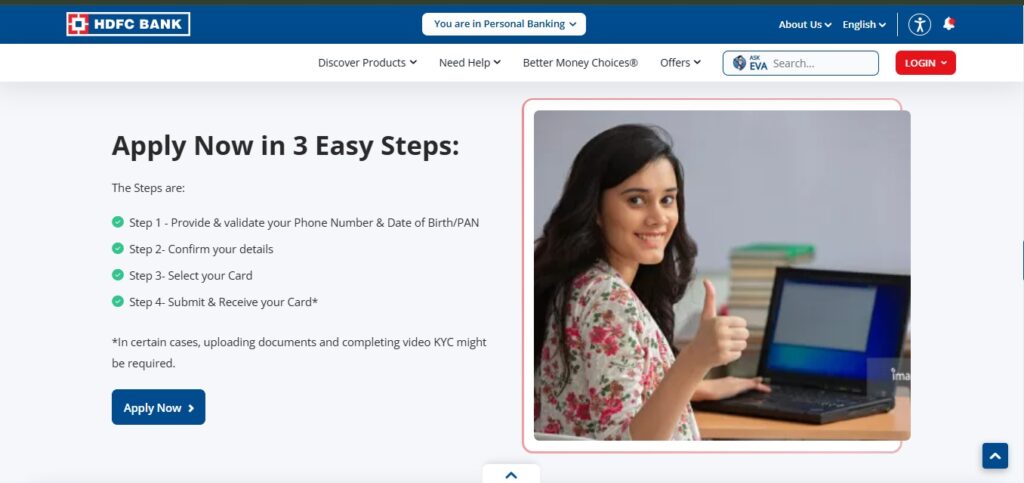

How to Apply and What You Need

The application process is pretty smooth:

- Go to the HDFC Bank website

- Fill out the online form — name, income details, basic personal info

- Upload your KYC documents — ID proof, address proof, income proof

- Once approved, the card arrives at your registered address, usually within a few business days

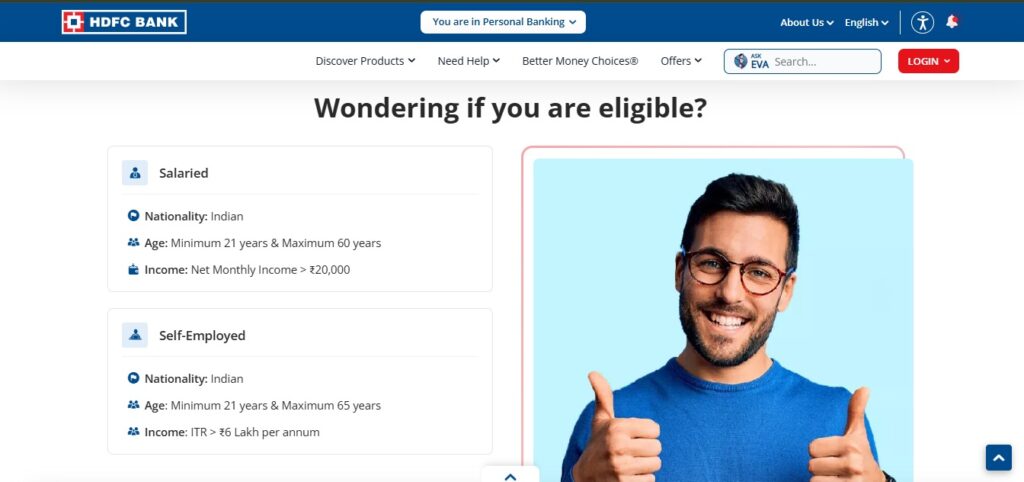

Who can apply for HDFC MoneyBack Credit Card:

- Age between 21 and 65

- A minimum income requirement (this varies depending on whether you’re salaried or self-employed)

- A decent credit history

If your credit score is in good shape and you have a stable income, the process shouldn’t give you much trouble.

How to Get the Most Out of This Card

Use It for Your Regular Expenses

Groceries, fuel, monthly bills — you’re spending on these anyway. Putting them on this card means points build up without any extra effort on your part.

Download the HDFC App

This isn’t just a suggestion. The app sends you alerts about promotions and bonus reward periods. Missing a bonus points campaign is like leaving free money on the table.

Plan Your Redemptions

Random, scattered redemptions don’t add up to much. Decide early — do you want cashback or vouchers? Is one bigger redemption at year-end better than smaller ones throughout the year? Having a simple plan makes a real difference.

Check Your Monthly Statement

It sounds boring, but it’s worth doing. Looking at your spending each month shows you where the card is working for you and where you can do better.

HDFC MoneyBack vs Other Reward Cards

| Feature | HDFC MoneyBack | HDFC Regalia | SBI SimplyCLICK | Axis Ace |

|---|---|---|---|---|

| Annual Fee | ₹500 (often waived) | ₹2,500 | ₹499 | ₹499 |

| Best For | Everyday cashback | Travel & lifestyle | Online shopping | Bill payments |

| General Reward Rate | 2 pts per ₹150 | 4 pts per ₹150 | 1 pt per ₹100 | 2% cashback |

| Cashback Option | ✅ Yes | ✅ Yes | ❌ No | ✅ Yes |

| Lounge Access | ❌ No | ✅ Yes | ❌ No | ❌ No |

| Fuel Surcharge Waiver | ✅ Yes | ✅ Yes | ❌ No | ✅ Yes |

| Reward Expiry | 2 years | 2 years | 2 years | No expiry |

| Ideal For Income | ₹2–4L/year | ₹6L+/year | ₹2–5L/year | ₹2–5L/year |

| Overall Value | ⭐⭐⭐ | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ |

Is Your Money Safe?

HDFC has the standard security features in place, and they work well:

- EMV Chip Technology — Much more secure than old magnetic stripe cards. Reduces the risk of counterfeit fraud significantly.

- Two-Factor Authentication — Extra verification for sensitive transactions. You get an SMS or app notification before anything goes through.

- Fraud Monitoring — Unusual transactions get flagged automatically. If something looks off, HDFC usually reaches out quickly.

One practical tip: turn on real-time transaction alerts in the app. It feels like a lot of notifications at first, but if an unauthorized charge ever shows up, you’ll know about it immediately.

Frequently Asked Questions

You earn points on every purchase — groceries, fuel, online shopping, and dining. Bonus points are available during festive season campaigns.

The annual fee is ₹500, often waived in the first year. After that, waiver depends on your annual spending. Check HDFC’s website for current terms.

You must be 21–65 years old, meet the minimum income requirement, and have a decent credit history.

Yes. Points can be converted to cashback and applied directly to your credit card bill.

Yes. Online transactions earn points like any other purchase, and HDFC SmartBuy portal sometimes offers extra rewards on online orders.

Bottom Line

The HDFC MoneyBack Credit Card won’t make you rich. But as a no-nonsense cashback card for everyday spending, it does its job well.

If you’re getting your first credit card, or you just want one reliable card that gives you real value without any complexity — this is a smart, practical choice.

Disclaimer: This article is for general information only. Before applying, please check HDFC Bank’s official website for the latest fees, terms, and eligibility criteria. Always make financial decisions based on your own situation.